Filing Taxes as a Widow

Filing Taxes as a Widow

The Ultimate Survival Guide for Widows

Welcome

Welcome

Section 2: Let's Get Organized

Section 2: Let's Get Organized

Section 3: Social Security Suvivor Benefits

Section 3: Social Security Suvivor Benefits

BONUS: Let's Do a Check-In

BONUS: Let's Do a Check-In

BONUS: The Ultimate Budget Binder for Widows

BONUS: The Ultimate Budget Binder for Widows

Section 5: Other Death Benefits

Section 5: Other Death Benefits

BONUS: The Ultimate Insurance Review for Widows

BONUS: The Ultimate Insurance Review for Widows

Section 8: Social Media + Online Accounts

Section 8: Social Media + Online Accounts

Section 9: What to Do With His Stuff

Section 9: What to Do With His Stuff

Master List

Master List

Whether you decide to tackle tax preparation yourself, or pay someone else to do it, you still need to keep track of all the tax documents arriving in your mailbox.

Free tax return preparation for qualifying taxpayers

If you are a low-to moderate-income, disabled or a limited English-speaking taxpayer, you can get free assistance with your tax preparation through the IRS Volunteer Income Tax Assistance (VITA) program.

Certified volunteers, working through grants from the IRS, provide free basic income tax return preparation with electronic filing to qualified individuals.

Click here for a list of schedules and forms the VITA program will and won’t prepare:

If you’re aged 60 or older, check out the Tax Counseling for the Elderly (TCE) program which offers free tax help for older taxpayers who often have pension and retirement-related questions unique to seniors.

Deceased’s final tax return

When you file your spouse’s final return, be sure to send a copy of the death certificate. This is used to notify the IRS and flag the account that the person is deceased.

Your new filing status

Your tax filing status will most likely change. The options for your tax filing status going forward are:

File jointly with your deceased spouse in the year of his death. That option is only available in the same year that he died.

If you have dependent children, you can file as "widow with dependent child" for two years following the year of death (unless you get remarried).

After two years, the filing status would change to single or Head of Household if you qualify.

I won’t go into the specifics of each filing option because I’m not a CPA or tax expert, but here are some articles that might be helpful:

What income documents to look for

After the beginning of the year, you will start receiving tax documents either in the mail, or electronically if you’ve opted out of snail mail service.

You will probably receive lots of tax documents and understanding what each document means can be very confusing.

I’ll give you a brief overview here of the common tax documents you’re likely to receive. If you’d like to check off documents as you receive them, use the following checklist to keep track.

Keep these income-related documents in your binder, so you know exactly where to look for them when you begin preparing your tax files.

Tax documents to expect:

W-2: If you are an employee and earned income from which social security taxes or Medicare tax was withheld, you will receive a W-2. This means you worked for someone else.

1099-MISC: If you’re self-employed or an independent contractor, you will receive a form 1099-MISC which reports any self-employment income of $600 or more. You will also receive a 1099-MISC for income received from rent, cash prizes or awards, or other services performed.

1099-INT: Reports interest income from accounts which pay you interest, like bank or investment accounts.

1099-DIV: Reports dividend income from stock or mutual fund investments. Dividends are earnings paid directly to shareholders.

1099-C: Reports any debt cancellation. Keep in mind that cancelled debt is still considered income, so you must pay taxes on it.

1099-G: Reports unemployment income which is subject to taxes. Box 1 shows the amount of your benefits. Box 4 shows the amount if you chose to have taxes withheld.

1099-R: Reports distributions from pensions, annuities, or retirement accounts.

1099-S: Reports distributions from real estate transactions (for example if you sell your house). This form will tell you what real estate income you must report to the IRS and pay taxes on.

1099-SA: Reports distributions from a Health Savings Account (HSA).

SSA-1099: Reports distributions from social security accounts.

All these documents report the income you or your spouse received. You must keep track of and report all your income.

If you receive a 1099 of any kind, SO DID THE IRS.

Make sure you include all the 1099s you received on your tax return.

The only exception to this rule is the SSA-1099 addressed to your child for child survivor benefits. If your children receive survivor benefits, you will get an SSA-1099 income statement addressed to both your child and you, as Representative Payee.

But you don’t pay taxes on your child’s benefits.

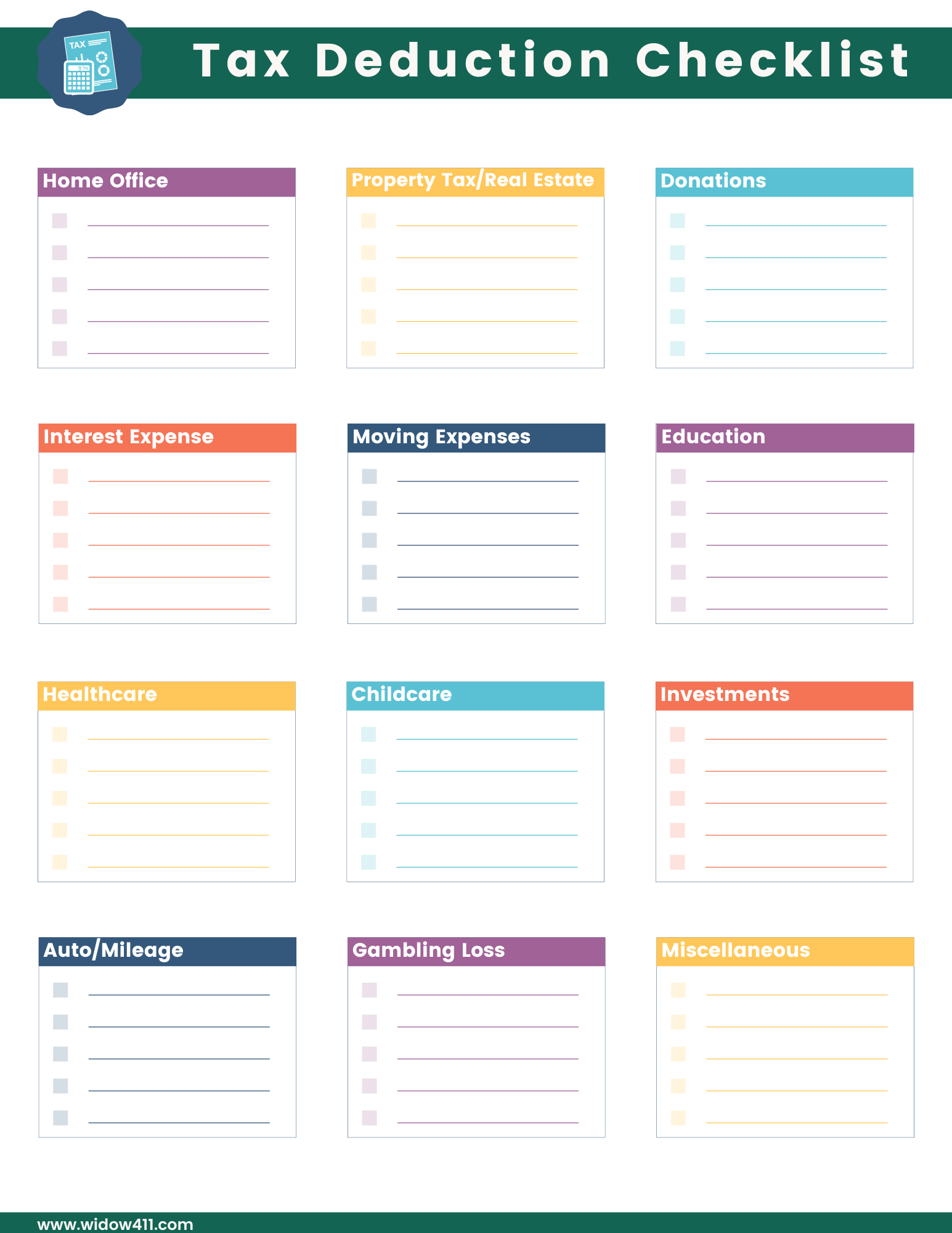

Take advantage of deductions and credits

You can deduct certain things to help lower your taxable income or apply for credits that directly reduce your taxes. Make sure you take advantage of the following ways to use deductions and credits.

See Credits and Deductions for Individuals for a complete list.

In order to claim the deduction or credit, you must show the IRS proof of your claim. Begin by collecting the following documents and keeping copies in your binder or separate tax folder to reach for when tax time rolls around.

Mortgage Interest Statement: Reports interest paid on your mortgage for the tax year which you can claim as a deduction on your taxes.

Property Tax applies only to the main home. Keep copies of both summer and winter tax payments.

Charitable Donations: Keep receipts for any cash amounts or value of donated property.

Childcare Costs: This is only for children under age 13 (or disabled at any age) and includes not only daycare costs but also costs of babysitters and summer day camps if those costs were incurred while you were at work (overnight summer camps don’t count).

Moving Expenses: Only if your expenses relate to moving for a new job or transferring current job.

Interest Expenses: Only applies to things like student loan interest, farm business interest, etc. Click here for more information on interest expenses and how you might qualify.

Home Based Business Expenses: If you use part of your home for business, you may be able to deduct expenses for the business use of your home. Click here for more information on home office deductions.

Work-Related Educational Expenses:Tax benefits might apply if you're saving for or paying education costs for yourself or, in many cases, another student who is a member of your immediate family. Click here for more information on tax benefits for education.

Deductions and credits are based on several criteria. Please be sure to do your due diligence and read all applicable guides if you’re preparing your own taxes.

Use this Tax Deduction Checklist to keep track of all your deductions. Download the worksheet and add it to your binder.

This worksheet is editable, which means you can enter/edit data right from your computer. Or simply download, print, and fill out by hand.

You'll find this document under the Downloads section below.

How to lower your AGI to pay fewer taxes

No one likes to pay taxes, so it’s essential that you know how to reduce your taxable income. When you lower your Adjusted Gross Income (AGI), you lower the amount you owe in taxes.

Yippee!

For example, I have a Health Savings Account (HSA) and any contributions I make to the HSA (please verify the current year's contributions ) lowers my AGI. To make this super simple, if you make 40,000 per year in gross income and you contribute the max to an HSA (in this example, we're using $6,900), you only pay taxes on $33,100 ($40,000 – $6,900 = $33,100).

If any of the following apply to you, make sure to take advantage of the income adjustments by providing the tax paperwork to your tax preparer or entering it on your tax software. You may receive some tax forms in the mail, or you may have to review purchase receipts to see if you qualify for any of these ways to lower AGI.

Make copies of any and all documents pertaining to these adjustments and keep them in your binder or tax folder.

You can reduce your adjusted gross income using the following tips:

HSA contributions (this comes on a 5498-SA Tax Form)

Health Insurance payments for self-employed (you take this deduction on Form 1040, line 29)

IRA contributions (based on limits if you’re also covered by a company plan)

Contributions to self-employed pension plans like SEP, etc. (deducted on Form 1040 on the line for self-employed SEP, SIMPLE, and qualified plans)

Student loan interest paid (form 1098-E)

Tuition paid (Form 1098-T)

Teachers – expenses paid for classroom supplies. Keep copies of receipts.

-

Energy Efficient Home Improvements – if you’ve replaced windows, furnace or air-conditioning units or your hot water heater, etc., keep all receipts and paperwork of energy efficient ratings. Contact your local electricity or natural gas provider to ask about rebates.